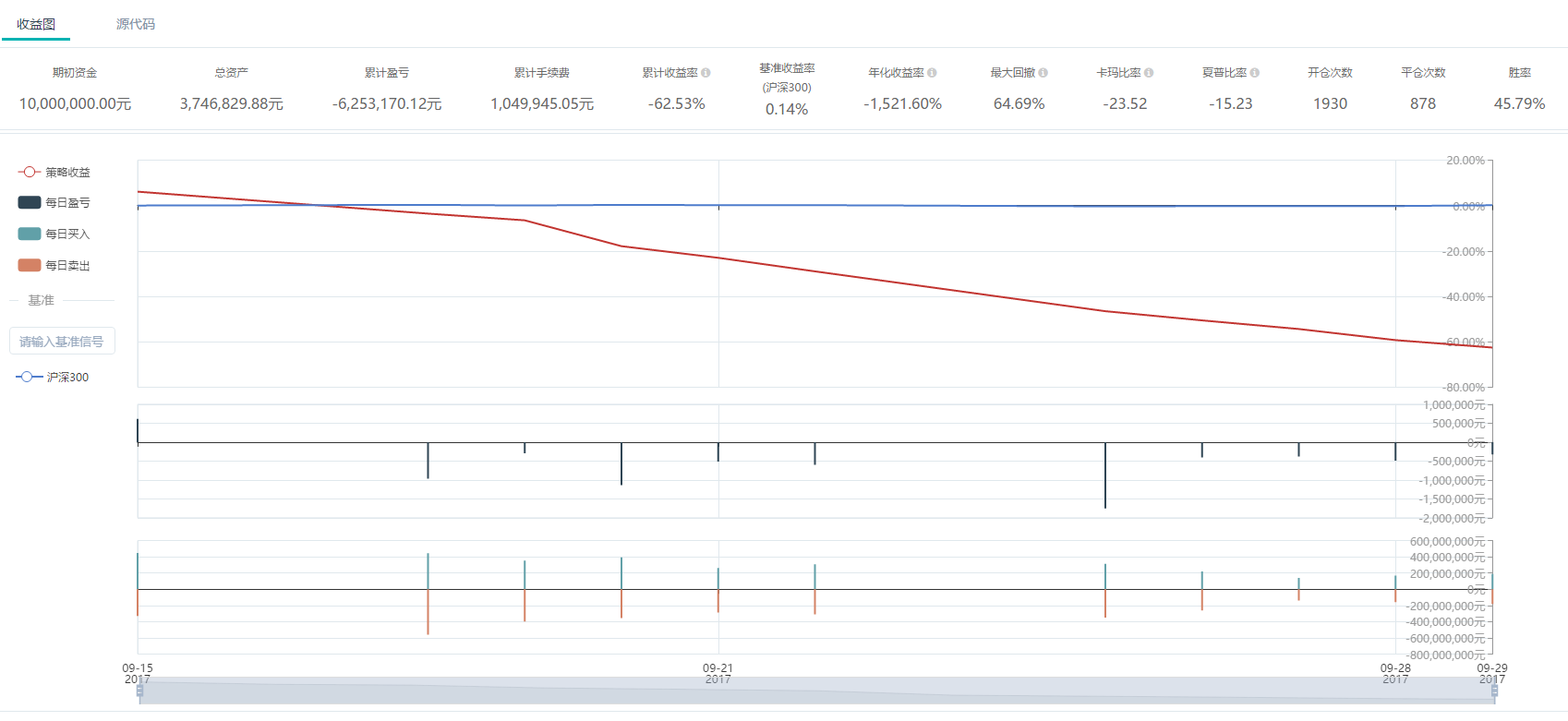

# coding=utf-8from __future__ import print_function, absolute_import, unicode_literalsimport numpy as npimport pandas as pdtry: import talibexcept: print('请安装TA-Lib库')from gm.api import *'''本策略通过计算CZCE.FG801和SHFE.rb1801的ATR.唐奇安通道和MA线,并:上穿唐奇安通道且短MA在长MA上方则开多仓,下穿唐奇安通道且短MA在长MA下方则开空仓若有 多/空 仓位则分别:价格 跌/涨 破唐奇安平仓通道 上/下 轨则全平仓位,否则根据 跌/涨 破持仓均价 -/+ x(x=0.5,1,1.5,2)倍ATR把仓位回测数据为:CZCE.FG801和SHFE.rb1801的1min数据回测时间为:2017-09-15 09:15:00到2017-10-01 15:00:00'''def init(context): # context.parameter分别为唐奇安开仓通道.唐奇安平仓通道.短ma.长ma.ATR的参数 context.parameter = [55, 20, 10, 60, 20] context.tar = context.parameter[4] # context.goods交易的品种 context.goods = ['CZCE.FG801', 'SHFE.rb1801'] # context.ratio交易最大资金比率 context.ratio = 0.8 # 订阅context.goods里面的品种, bar频率为1min subscribe(symbols=context.goods, frequency='60s', count=101) # 止损的比例区间def on_bar(context, bars): bar = bars[0] symbol = bar['symbol'] recent_data = context.data(symbol=symbol, frequency='60s', count=101, fields='close,high,low') close = recent_data['close'].values[-1] # 计算ATR atr = talib.ATR(recent_data['high'].values, recent_data['low'].values, recent_data['close'].values, timeperiod=context.tar)[-1] # 计算唐奇安开仓和平仓通道 context.don_open = context.parameter[0] + 1 upper_band = talib.MAX(recent_data['close'].values[:-1], timeperiod=context.don_open)[-1] context.don_close = context.parameter[1] + 1 lower_band = talib.MIN(recent_data['close'].values[:-1], timeperiod=context.don_close)[-1] # 计算开仓的资金比例 percent = context.ratio / float(len(context.goods)) # 若没有仓位则开仓 position_long = context.account().position(symbol=symbol, side=PositionSide_Long) position_short = context.account().position(symbol=symbol, side=PositionSide_Short) if not position_long and not position_short: # 计算长短ma线.DIF ma_short = talib.MA(recent_data['close'].values, timeperiod=(context.parameter[2] + 1))[-1] ma_long = talib.MA(recent_data['close'].values, timeperiod=(context.parameter[3] + 1))[-1] dif = ma_short - ma_long # 获取当前价格 # 上穿唐奇安通道且短ma在长ma上方则开多仓 if close > upper_band and (dif > 0): order_target_percent(symbol=symbol, percent=percent, order_type=OrderType_Market, position_side=PositionSide_Long) print(symbol, '市价单开多仓到比例: ', percent) # 下穿唐奇安通道且短ma在长ma下方则开空仓 if close < lower_band and (dif < 0): order_target_percent(symbol=symbol, percent=percent, order_type=OrderType_Market, position_side=PositionSide_Short) print(symbol, '市价单开空仓到比例: ', percent) elif position_long: # 价格跌破唐奇安平仓通道全平仓位止损 if close < lower_band: order_close_all() print(symbol, '市价单全平仓位') else: # 获取持仓均价 vwap = position_long['vwap'] # 获取持仓的资金 money = position_long['cost'] # 获取平仓的区间 band = vwap - np.array([200, 2, 1.5, 1, 0.5, -100]) * atr grid_percent = float(pd.cut([close], band, labels=[0, 0.25, 0.5, 0.75, 1])[0]) * percent # 选择现有百分比和区间百分比中较小的值(避免开仓) target_percent = np.minimum(money / context.account().cash['nav'], grid_percent) if target_percent != 1.0: print(symbol, '市价单平多仓到比例: ', target_percent) order_target_percent(symbol=symbol, percent=target_percent, order_type=OrderType_Market, position_side=PositionSide_Long) elif position_short: # 价格涨破唐奇安平仓通道或价格涨破持仓均价加两倍ATR平空仓 if close > upper_band: order_close_all() print(symbol, '市价单全平仓位') else: # 获取持仓均价 vwap = position_short['vwap'] # 获取持仓的资金 money = position_short['cost'] # 获取平仓的区间 band = vwap + np.array([-100, 0.5, 1, 1.5, 2, 200]) * atr grid_percent = float(pd.cut([close], band, labels=[1, 0.75, 0.5, 0.25, 0])[0]) * percent # 选择现有百分比和区间百分比中较小的值(避免开仓) target_percent = np.minimum(money / context.account().cash['nav'], grid_percent) if target_percent != 1.0: order_target_percent(symbol=symbol, percent=target_percent, order_type=OrderType_Market, position_side=PositionSide_Short) print(symbol, '市价单平空仓到比例: ', target_percent)if __name__ == '__main__': ''' strategy_id策略ID,由系统生成 filename文件名,请与本文件名保持一致 mode实时模式:MODE_LIVE回测模式:MODE_BACKTEST token绑定计算机的ID,可在系统设置-密钥管理中生成 backtest_start_time回测开始时间 backtest_end_time回测结束时间 backtest_adjust股票复权方式不复权:ADJUST_NONE前复权:ADJUST_PREV后复权:ADJUST_POST backtest_initial_cash回测初始资金 backtest_commission_ratio回测佣金比例 backtest_slippage_ratio回测滑点比例 ''' run(strategy_id='strategy_id', filename='main.py', mode=MODE_BACKTEST, token='token_id', backtest_start_time='2017-09-15 09:15:00', backtest_end_time='2017-10-01 15:00:00', backtest_adjust=ADJUST_PREV, backtest_initial_cash=10000000, backtest_commission_ratio=0.0001, backtest_slippage_ratio=0.0001)

原文: https://www.myquant.cn/docs/python_strategyies/110